Protecting Your Home Starts Here

Your home deserves thoughtful, comprehensive protection — and that’s exactly what TGS Insurance delivers. As an independent agency, we’re not tied to one carrier, which means our recommendations are built around your best interests. We evaluate coverage details carefully, identify opportunities for discounts, and help you avoid gaps that could leave you exposed. The result? A policy designed with care, backed by expertise, and built to protect what matters most.

Building the Right Home Insurance in Lake Charles

Selecting homeowners insurance in Lake Charles isn’t just about meeting lender requirements — it’s about ensuring long-term protection. A typical Lake Charles home insurance policy provides:

- Structural protection for your home

- Coverage for personal belongings

- Liability safeguards

- Coverage for additional living expenses

- Optional endorsements tailored to your property

Many homeowners exploring home insurance in Lake Charles also consider add-ons like water backup coverage, scheduled personal property, or extended replacement cost coverage to avoid gaps. Reviewing these options helps create a more complete Lake Charles home insurance plan.

How Much Does Home Insurance Cost in Lake Charles?

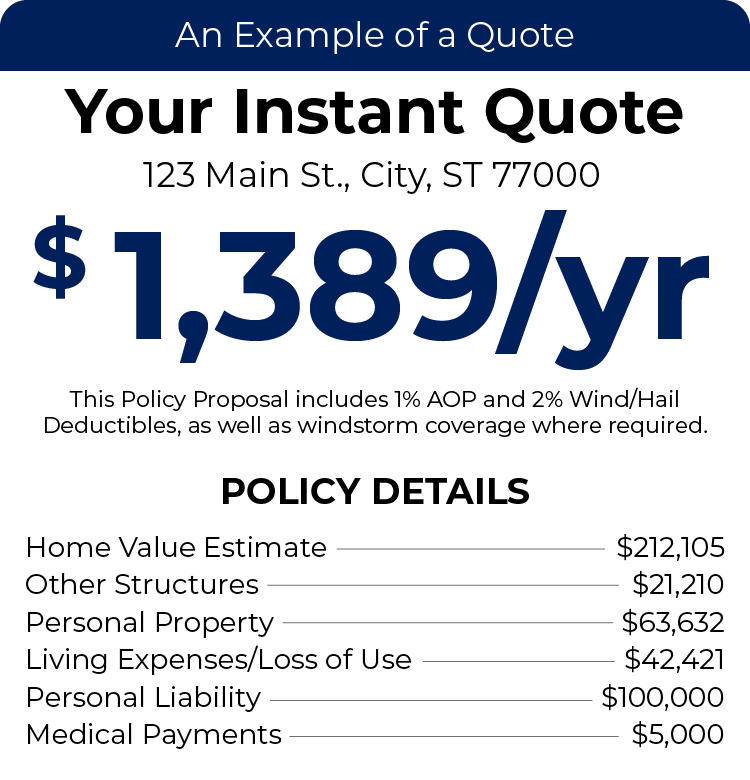

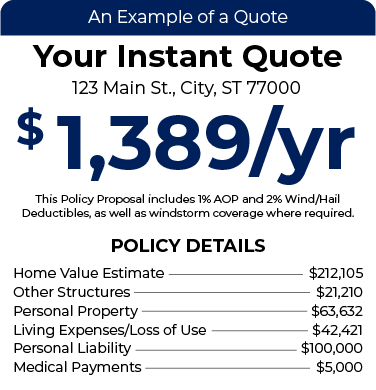

For homeowners in Lake Charles, the average annual premium with TGS Insurance is $2,714. That number is based on policies written for homes with an average value of $339,952 and includes wind and hail coverage with a 2% deductible.

Of course, your rate won’t be identical to anyone else’s. Your home’s age, construction type, location, credit profile, and the coverage limits you select all play a role in shaping your premium. The good news? You’re in control. Coverage can be adjusted to match both your protection needs and your budget. Enter your address above to see your personalized quote in minutes.

Average Home Insurance Premiums in Lake Charles by Dwelling Coverage

Dwelling coverage is the portion of your home insurance policy that protects the structure of your home itself — walls, roof, foundation, and built-in features — if a covered loss occurs. The limit you select should reflect what it would realistically cost to rebuild your home at today’s construction prices, not what you paid for it.

Because the insurer is agreeing to potentially pay up to that limit, your dwelling coverage amount directly affects your premium. Higher limits typically mean higher premiums.

Dwelling Coverage Limits Average Annual Premium (incl. Windstorm & Hail Coverage)

$100,000 - $200,000 $1,914

$200,000 - $300,000 $2,206

$300,000 - $400,000 $2,620

$400,000 - $500,000 $3,459

$500,000 - $600,000 $4,228

$600,000 - $700,000 $5,084

Why Home Insurance Costs Differ by Neighborhood in Lake Charles

Not every homeowner in Lake Charles pays the same rate — even within the same city limits. Your exact location can significantly influence your premium, sometimes down to the zip code.

Insurers evaluate localized risk when determining pricing. That includes neighborhood crime statistics, storm exposure, historical claims data, and proximity to emergency services. Rebuilding costs can also vary by area, especially if labor and materials are more expensive in certain parts of Lake Charles.

In fact, the zip code with the highest average premium in Lake Charles is 70605, where homeowners pay around $3,146 per year on average. This reflects how hyper-local risk factors can shape insurance pricing.

Does the Age of Your Home Impact Insurance in Lake Charles?

Yes — and sometimes more than homeowners expect. Insurance carriers evaluate a property’s age because it helps them estimate the likelihood of future repairs or claims.

Older homes in Lake Charles may have aging roofs, outdated wiring, or plumbing systems that increase the chance of fire or water damage. Even if the home has been well maintained, insurers often price policies based on statistical risk tied to older construction.

In contrast, newly built homes usually meet current safety codes and are constructed with materials designed for durability. Because they tend to experience fewer large-scale claims early on, premiums for newer homes are often lower than those for older properties.

Does Square Footage Change Your Lake Charles Home Insurance Premium?

Yes — and sometimes significantly. Insurance companies base part of your premium on what it would cost to fully rebuild your home. As square footage increases, so does the estimated reconstruction cost.

Bigger homes often involve:

- More construction materials

- Higher labor expenses

- Larger roof surfaces

- Expanded electrical and plumbing systems

All of these increase the insurer’s potential financial exposure.

For homeowners in Lake Charles, properties larger than 2,500 square feet average $3,818 per year in premiums. Homes under 2,500 square feet average $2,397. The difference reflects the increased cost to insure larger structures.

Why Quotes Can Vary for the Same Home

If you’ve ever received two very different quotes for the same property, you’re not alone. Home insurance pricing isn’t one-size-fits-all across companies.

Carriers analyze data differently. Some rely heavily on historical claims trends in a specific area. Others may focus more on individual property characteristics like roof age or home updates. Discount availability also varies — what earns savings with one company may not with another.

Additionally, some insurers build more comprehensive coverage into their base policy, while others offer leaner base policies at lower starting prices. That variation can create noticeable differences in premium.

Lake Charles Areas We Cover

- 70601

- 70602

- 70605

- 70606

- 70607

- 70609

- 70615

- 70616

- 70629

Live in a zip code that’s not shown? We’ve still got you covered. Our team helps homeowners all across Louisiana compare home insurance options and find the right fit. Begin with your free instant quote by entering your address above.