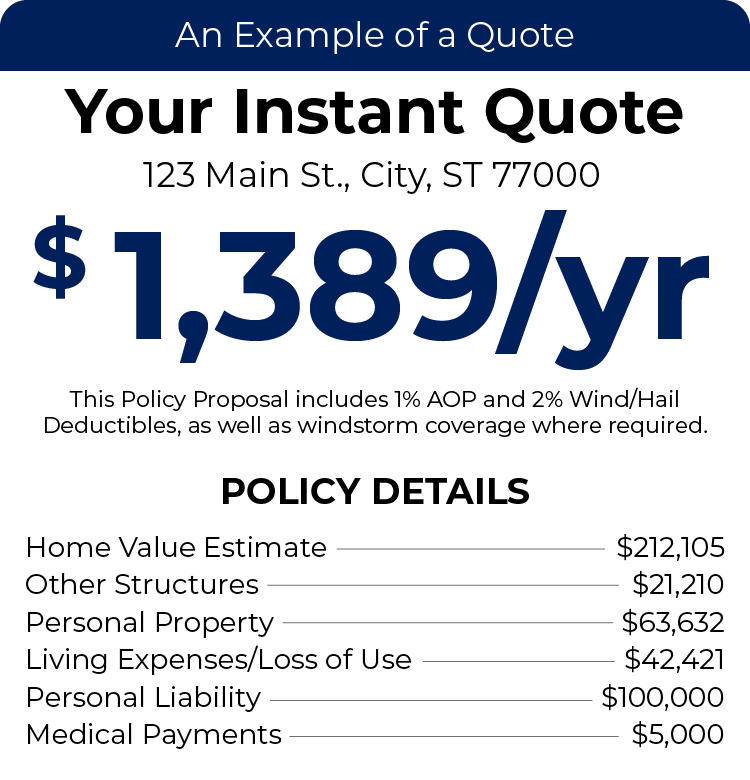

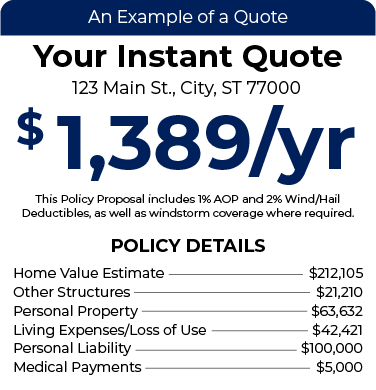

Instant Home Insurance Quote

All We Need Is Your Address, NO BS!

See What Our Clients Have to Say

Excellent

Based on 3,313 reviews

Texas Homeowners Insurance

Your home is more than just a place to live—it’s your safe haven, your investment, and where life’s best moments happen. Protecting it with the right homeowners insurance gives you peace of mind knowing that no matter what life brings, your home and everything in it are covered. At TGS Insurance, we make finding affordable Texas homeowners insurance simple. Our experts compare quotes from top-rated carriers to help you secure the protection you need without overpaying—so you can focus on enjoying the place you call home.

What Does Texas Homeowners Insurance Cover?

Homeowners insurance offers coverages that are designed to help you protect your home, personal belongings, and your liability should your home become a victim of specified perils including a visitor’s medical bills, fire, theft/vandalism, etc. Policies vary, but take a look at some of the most common coverage options below:

- Dwelling Coverage: this protects your home’s physical structures such as your home’s foundation, roof, and walls. It can even protect structures that are connected to your home such as a deck, detached garage, or patio. Dwelling coverage is a fundamental coverage of homeowners insurance.

- Loss of Use/Additional Living Expenses Coverage: should a covered peril create a situation in which your home is unlivable, this coverage helps you pay for where you temporarily reside while waiting for your home to be rebuilt to a livable condition.

- Medical Expenses Coverage: a part of your homeowners insurance policy that helps cover the necessary medical bills of a guest in your home should someone become injured while visiting your property. Medical expenses coverage can even help offset costs if you are not at fault.

- Other Structures Coverage: while the main structure of your home is covered by dwelling coverage, structures that are not connected to your home will need other structures coverage to stay protected. This includes decks, detached garages, sheds/shops, and more.

- Personal Liability Coverage: this coverage is to protect homeowners against possible medical costs that can accumulate should a visiting party become injured on your property and you are found to be at fault. Personal liability coverage can also cover potential legal fees associated with the injury.

- Personal Property Coverage: protects against damaged personal property that occurs from specified perils including fires, theft, or vandalism. Each policy varies and what is or isn’t covered will depend on your insurance provider. For more expensive items such as art or jewelry, you may require extended coverage options.

In addition to these policy coverage options, many homeowners elect to add endorsements or riders to their insurance policies to fill in gaps that may exist when relying on a standard policy alone.

- Equipment Breakdown Coverage: a way to protect important appliances under the same policy against breaking down due to a fault of the manufacturer such as an electrical or mechanical failure. Equipment breakdown coverage does not protect against the natural wear and tear of an appliance.

- Personal Property Replacement Cost Coverage: additional coverage that helps protect personal property from being destroyed or stolen under the provided coverage terms of your policy. Remember, items such as expensive artwork or precious metals may require more than a standard policy. Personal property replacement cost coverage mitigates your replacement costs.

- Water/Sewer Backup Coverage: if your home’s sewage or drains should become backed up into your home, this coverage protects you from the costs of the damages that occurred, fixing the problem, and even damage from mold caused by these backups.

Is Homeowners Insurance Required in Texas?

Homeowners insurance isn’t required by law in Texas, but most mortgage lenders will require coverage up to the full value of your home to protect their financial interest. Even if your home is fully paid off, maintaining a homeowners policy is strongly recommended. Without insurance, a single disaster—such as a fire, storm damage, or theft—could leave you facing overwhelming repair or replacement costs on your own.

From everyday risks like roof damage from lightning to major losses caused by severe weather, the right homeowners insurance policy helps safeguard your home and finances.

How Much Does Texas Home Insurance Cost?

The average Texas homeowners insurance cost is over $3,400 per year, making it one of the highest in the nation. With severe weather risks, rising home values, and evolving coverage needs, it’s easy to see why Texas ranks among the top five most expensive states for home insurance. But that doesn’t mean you’re stuck paying sky-high rates. At TGS Insurance, we help Texans save an average of $870 a year by comparing quotes from our network of top-rated insurance carriers. In just seconds, you can find out how much you could save through our instant online quote tool or by connecting with one of our licensed agents, who are always ready to find you the right coverage at the best price.

What Impacts the Cost of Your Homeowners Insurance?

Your home insurance rate is shaped by a variety of personal and property-specific factors. Insurers represented by TGS Insurance Agency evaluate key details such as the age, location, and value of your home, your credit score, and even the number of people living in your household. Homes in coastal or storm-prone regions often see higher premiums due to increased weather-related risks, while newer homes or those with strong safety features may qualify for discounts. Once we gather your information, our team crafts a personalized homeowners insurance quote and matches you with the provider that best balances affordable pricing and reliable protection—so you can get the coverage you deserve without paying more than you should.

How to Buy Homeowners Insurance

Buying the right homeowners insurance is one of the most important steps in protecting your home, family, and belongings. But finding the right insurance provider can make all the difference in cost and coverage. At TGS Insurance, we’ve been helping Texans save on home insurance since 2017 by comparing quotes from over 55 top-rated carriers across the state. Our experts make the process simple—whether you’re a first-time homeowner or looking to switch providers for better savings.

You can even bundle your home and auto insurance to maximize discounts and simplify your protection under one roof. Get started today by contacting TGS Insurance for a fast, customized quote and discover how much you could save on your homeowners policy.

Learn More About Home Insurance on Our Blog:

Causes for Home and Auto Insurance Rate Increases in 2022

Actual Cash Value vs Replacement Cost

Comparing HO2 and HO3 Policies

Comparing HO3 and HO5 Policies

Comparing HO2 and HO5 Policies

Does a New Roof Lower Home Insurance?

More Articles on Home Insurance

Looking for More Information on Your Area?

Jersey Village Homeowners Insurance

Missouri City Homeowners Insurance

Sugar Land Homeowners Insurance

The Woodlands Homeowners Insurance

San Antonio Homeowners Insurance

Not In Texas?

TGS Insurance now offers:

Home Insurance FAQs

What do I need to get a homeowners insurance quote?

Getting a quote is simple! You’ll just need your home’s address, year built, square footage, roof type, and details about any updates or renovations. Having your current insurance policy on hand also helps when comparing coverage and savings.

How many homeowners insurance quotes should I get?

It’s a good idea to compare at least three quotes to make sure you’re getting the best rate and coverage. Many independent agencies can shop your policy with multiple top-rated carriers at once to save you time and effort.

How do I compare homeowners insurance quotes?

When comparing quotes, look beyond the price tag. Make sure coverage limits, deductibles, and included protections align. The cheapest option isn’t always the best if it leaves you underinsured when you need it most. Reviewing each quote side by side can help you make an informed choice.

Can I bundle my homeowners insurance with my auto policy?

Yes! Bundling your home and auto insurance can save you money and make managing your policies easier. Most carriers offer multi-policy discounts when you combine your coverage under one provider.

How often should I review my homeowners insurance policy?

Review your policy once a year or anytime you make significant home changes, like remodeling, adding a pool, or purchasing valuable items. Keeping your coverage up to date ensures your home stays properly protected.

What affects the cost of my homeowners insurance?

Several factors influence your premium, including your home’s age, condition, and location, as well as your roof type, rebuild cost, and claims or credit history. Local risks like hurricanes or hail also play a role. Reviewing your coverage regularly can help you find savings opportunities.