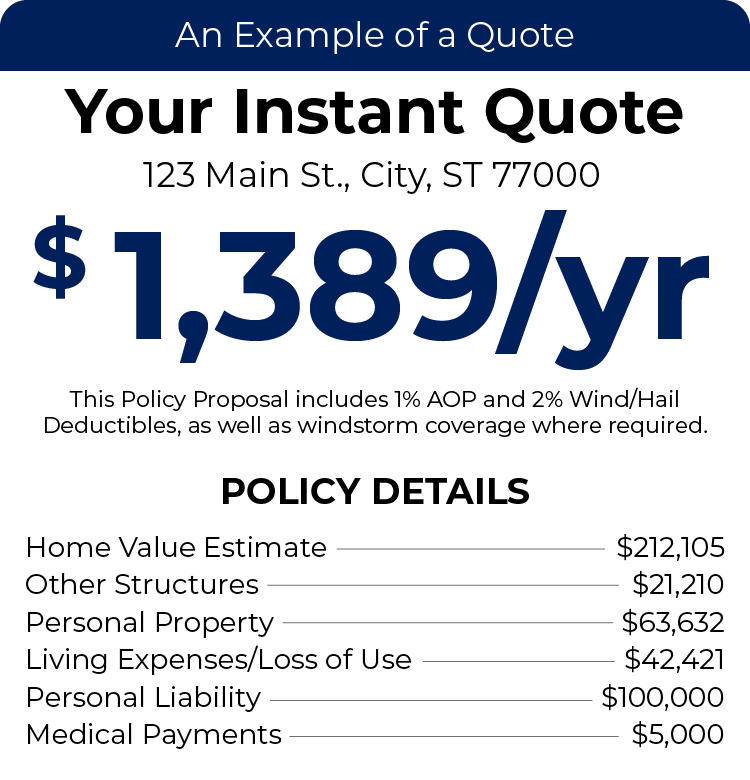

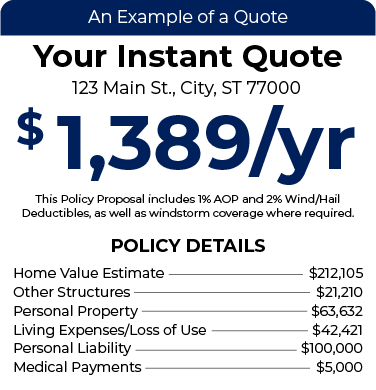

Instant Home Insurance Quote

All We Need Is Your Address, NO BS!

What is Personal Liability on Homeowners Insurance?

Personal liability coverage is a component of your homeowners insurance policy. It pays for any bodily injury or property damage claims made against you or members of your household where you are legally liable. While you hope you’re never held responsible for an accident, this coverage helps you avoid paying out-of-pocket for unexpected damages. So, let’s review what’s included in your homeowners personal liability coverage and how it works to protect you and your family.

Liability Coverage: Bodily Injury & Property Damage

Homeowners liability coverage breaks down into two components. These are bodily injury and property damage for which either you or a home member are responsible. Examples of both include:

- Bodily injury: a visitor takes a tumble down your stairs, requires medical attention, and misses work. They can sue you for medical bills, lost wages, and distress. Consequently, without personal liability coverage (or enough), you could be responsible for paying out-of-pocket expenses if you’re legally liable.

- Personal property: during a thunderstorm, a tree from your property gets knocked over. It falls onto your neighbor’s home, damaging their roof. Your neighbor could sue you for damages. Again, if you’re found responsible, you’d be on the hook to pay the bill if you didn’t have the proper liability coverage.

What Does Personal Liability Homeowners Insurance Cover?

Personal liability provides financial protection for you and the members of your household. These coverages can include:

- Damage to Other’s Property: This applies if you or your household relatives are at fault for the damage. For example, if your child throws a baseball over the fence and breaks your neighbor’s window.

- Injuries on your property: If you are legally responsible, your personal property coverage may help pay for someone else’s injuries that occur on your property- up to the limits on your policy.

- Lawsuits and lawyer/court fees: If the guest sues you over an accident, your personal liability coverage may help pay for a lawyer and legal expenses and any settlements against you.

What Isn’t Included Under Personal Liability?

Your homeowners insurance will cover personal injuries if your policy includes personal liability coverage, which most do. Some personal liability claims may not be covered, including:

- Business claims: Any claims against you that relate to your business or profession are not covered.

- Car accidents: Your auto liability insurance, rather than your personal liability coverage, covers you for damages or injuries caused while driving.

- Intentional harm or damages: Injuries or damages you or a household member purposely cause to someone else are not covered.

- Your injuries or damages: This coverage DOES NOT apply to accidents you cause to yourself or your family.

How Much Personal Liability Coverage Do I Need?

Homeowners should carry between $300,000-$500,000 worth of liability coverage, with the minimum amount being $100,000, according to the Insurance Information Institute. It’s essential to consider your net worth. The more financial assets you have, the more coverage you should carry to mitigate any risk of financial loss should someone sue you.

For example, suppose your net worth is $300,000, and an injured guest sues you for $200,000 but you only carry $100,000 in coverage. In that case, the plaintiff can come after any assets you have to compensate for the remaining $100,000 worth of damage.

TGSI Tip: If you have assets that total more than $100,000, we recommend carrying an umbrella policy or personal excess liability insurance. This serves as a form of supplemental coverage with a higher limit. These policies will help once you’ve exhausted your home insurance coverage limits.

In the scenario above, if you had these policies in place, they would help keep your assets safe!

It would be best if you also considered how risky your property is. Do you have a trampoline? A swimming pool? These additions to your space are attractive nuisances because they raise the potential for injury. You may consider increasing your personal liability coverage if you have these attractions in your yard.

TGS Insurance Can Help Keep You Financially Covered

Talk to a TGS Insurance agent today about your homeowner insurance policy. Learn more about your liability coverage options to safeguard you and your financial assets from the unexpected. See why over 15,000 Texans use TGS Insurance by getting your hassle-free home insurance quote now! It takes 15 seconds or less, and all we need is your address.

Explore Other Homeowners Insurance Coverages:

Recent Homeowners Insurance Articles:

- Thanksgiving Fire Safety: Protect Your Home, Your Family, and Your Peace of Mind

- Fall Home Maintenance Checklist: Prevent Costly Insurance Claims Before Winter

- Who Needs to be Listed on Homeowners Insurance

- Does Homeowners Insurance Cover Mold?

- Actual Cash Value vs. Replacement Value: What’s the Difference, and Where Does Market Value Fit In?