Protecting Your Home Starts Here

Your home deserves thoughtful, comprehensive protection — and that’s exactly what TGS Insurance delivers. As an independent agency, we’re not tied to one carrier, which means our recommendations are built around your best interests. We evaluate coverage details carefully, identify opportunities for discounts, and help you avoid gaps that could leave you exposed. The result? A policy designed with care, backed by expertise, and built to protect what matters most.

Oakdale Home Insurance Coverage Options Explained

When shopping for Oakdale home insurance, understanding your coverage options is key to protecting your property and your finances. A standard Oakdale home insurance policy is designed to provide multiple layers of protection, helping homeowners recover after covered losses such as fire, wind, theft, or certain types of water damage.

Most Oakdale home insurance policies include:

- Dwelling Coverage – Pays to repair or rebuild the structure of your home after a covered event.

- Other Structures Coverage – Protects detached garages, fences, sheds, and similar structures on your property.

- Personal Property Coverage – Helps replace furniture, electronics, clothing, and other belongings.

- Personal Liability Protection – Covers legal and medical expenses if someone is injured on your property.

- Loss of Use Coverage – Helps cover temporary housing and additional living expenses if your home becomes uninhabitable.

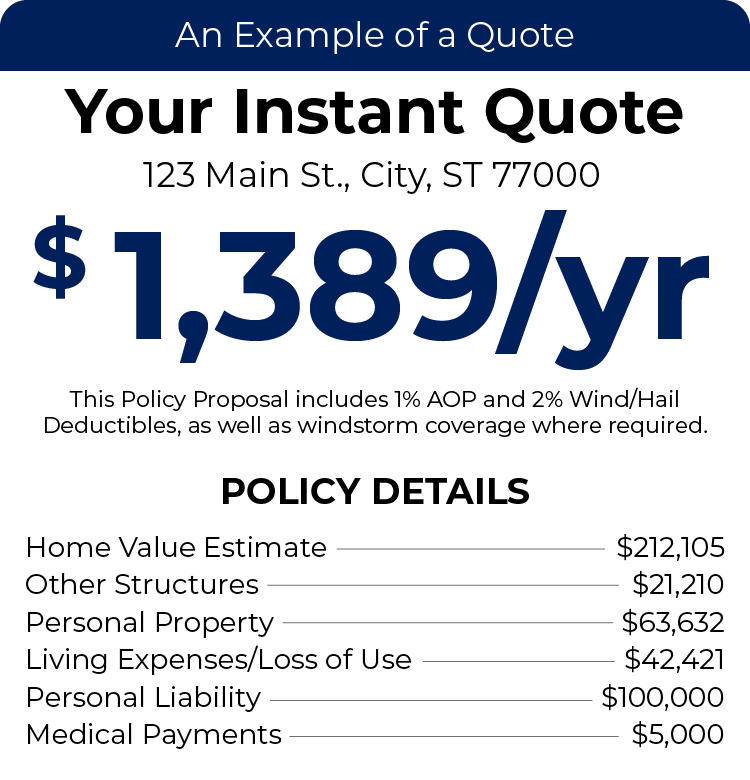

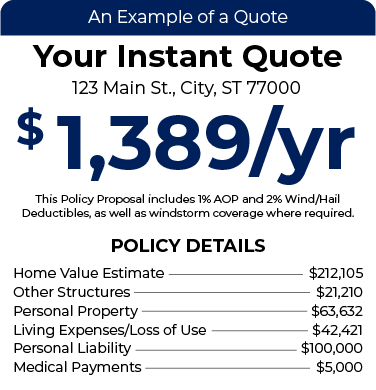

Depending on your property type, neighborhood, and specific risk factors, your Oakdale home insurance policy may also include optional endorsements such as water backup coverage, extended replacement cost coverage, or scheduled coverage for high-value items. Reviewing your Oakdale home insurance coverage limits and deductibles carefully ensures your policy aligns with your home’s true value and your financial goals.

What’s the Typical Home Insurance Premium in Oakdale?

The average TGS homeowner in Oakdale pays $1,351 per year for coverage. That figure assumes an average home value of $292,144 and includes windstorm and hail protection with a 2% deductible.

But averages only tell part of the story. Louisiana homes can vary widely in age, size, and exposure to weather-related risk — and those differences matter. Your premium will reflect details specific to your property, along with your chosen coverage levels and deductible preferences. A tailored quote will always give you the most accurate picture of what you can expect to pay.

How Dwelling Coverage Limits Affect Home Insurance Costs in Oakdale

One of the biggest drivers of your homeowners insurance premium is your dwelling coverage limit. This is the maximum amount your policy will pay to rebuild your home after a covered total loss.

Choosing the right limit is important — too low, and you risk being underinsured. Too high, and you may be paying more in premium than necessary. Since the coverage amount represents the insurer’s financial exposure, larger limits generally increase annual costs.

Dwelling Coverage Limits Average Annual Premium (incl. Windstorm & Hail Coverage)

$100,000 - $200,000 $930

$200,000 - $300,000 $1,229

$300,000 - $400,000 $1,510

$400,000 - $500,000 $1,851

$500,000 - $600,000 $2,327

Finding the right balance between protection and affordability starts with an accurate rebuild estimate.

How Home Age Affects Home Insurance Rates in Oakdale

The year your home was built can have a noticeable impact on your insurance premium. In Oakdale, older homes often cost more to insure because aging systems — like plumbing, electrical wiring, and HVAC — may present a higher risk of claims. Roof condition also becomes increasingly important as homes age, especially in areas prone to severe weather.

That difference is reflected in premium trends as well. Homes built within the last 25 years see an average premium of around $1,191, while homes built between 26 and 50 years ago average closer to $1,382. Older construction materials, outdated systems, and higher repair costs can all contribute to the increase.

Additionally, homes built decades ago may not meet today’s building codes or wind mitigation standards, which can increase potential repair costs after a loss.

Newer homes, on the other hand, typically benefit from updated materials, modern construction practices, and improved safety features. These upgrades often reduce the likelihood of major claims, which can translate into more favorable insurance rates.

How Home Size Impacts Insurance Costs in Oakdale

The square footage of your home directly influences how much you’ll pay for homeowners insurance. Simply put, larger homes cost more to rebuild. More space means more roofing materials, flooring, framing, and labor — all of which increase the potential claim payout after a covered loss.

Beyond rebuilding costs, larger homes often require higher personal property limits and may include additional features like upgraded kitchens, multiple HVAC systems, or expanded plumbing networks. These factors contribute to higher premiums.

In Oakdale, TGS customers with homes over 2,500 square feet pay an average of $2,116 per year. Homeowners with properties under 2,500 square feet pay an average of $1,234 annually, highlighting how size plays a meaningful role in insurance pricing.

Location Plays a Big Role in Oakdale Home Insurance Rates

Two homes with similar values in Oakdale can have very different premiums — simply because they sit in different zip codes.

Insurance companies analyze small-area data when setting rates. Factors like prior storm losses, flood exposure, theft trends, and even fire station response times can influence what you pay. Construction costs and property values within specific neighborhoods also help determine pricing.

Currently, 71463 carries the highest average premium in Oakdale, at approximately $1,351 per year. This highlights how much your specific address matters when calculating your home insurance rate.

Comparing Home Insurance Carriers: What Sets Them Apart?

Every insurance company has its own underwriting guidelines and risk tolerance. That means one carrier may view your home as a moderate risk, while another may classify it differently based on internal data models.

Carriers also differ in:

- How they assess storm exposure

- How they price prior claims

- What discounts they offer

- How flexible their coverage options are

Because each company’s formula is unique, premiums naturally vary. Shopping across multiple carriers helps ensure you’re seeing the full range of available pricing.

Home Insurance Coverage Across Oakdale

- 71463

If your zip code isn’t mentioned, you’re still in the right place. We proudly assist homeowners across Louisiana in finding reliable home insurance coverage. Start your free instant quote by typing in your address above.