Protecting your home with insurance is a must regardless of whether you rent or own it. Depending on your living situation, you’ll need either a renter or a homeowners insurance policy. Both, at the core, protect the policyholder’s personal property and any liability costs, but the biggest difference is what they don’t cover. Let’s break down renters insurance vs. homeowners insurance and how they differ in terms of price and coverage.

Renters vs. Homeowners Insurance

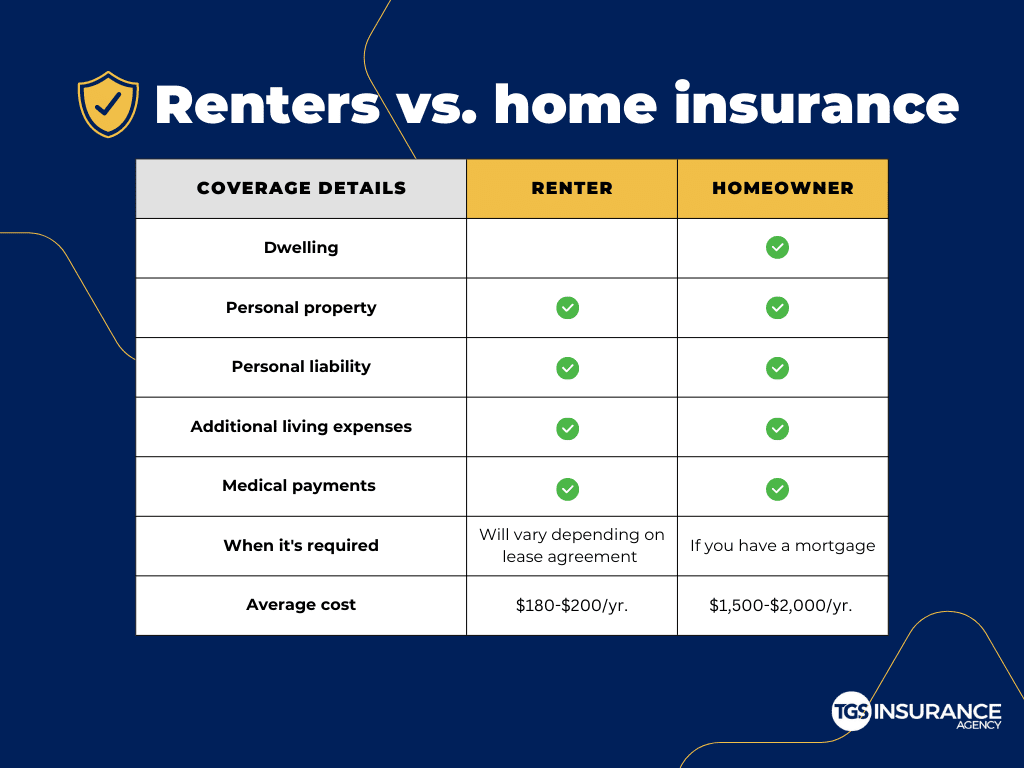

Renters vs. Homeowners Insurance Coverage

When you slice it up, home insurance and renters insurance are the same things with one exception. Both home and renter policies cover the following:

- Personal property

- Personal liability

- Additional living expenses

- Medical payments

The critical difference between a renters and homeowners insurance policy is dwelling coverage, aka the physical structure of your home. Renters are typically responsible for everything inside their home, whereas a landlord will cover any damage to the building or rented unit through their landlord insurance policy.

Homeowners and renters insurance policies have the same covered and excluded perils. Both types of policies will cover the following:

- Damage by aircraft or vehicles (excluding your own)

- Damage from water or steam-heating appliances

- Explosions

- Falling objects

- Fire

- Freezing of air conditioning, heating, and plumbing

- Hail

- Lighting

- Riots

- Short-circuit damage from electrical appliances

- Smoke damage

- Theft

- Vandalism

- Volcanic eruption

- Weight of ice, sleet, and snow

- Windstorm

Excluded perils include earthquakes, flooding, maintenance issues, mold or fungus growth, negligence, normal wear and tear, and pest or rodent infestation. In most cases, you’ll need a separate standalone policy for perils such as floods or earthquakes.

Renters vs. Homeowners Insurance Cost

Home insurance is more expensive than renters insurance because home insurance includes the cost to insure the dwelling and any other attached structures. (I.E., a detached garage or fence.) On average, renters insurance can cost anywhere between $15 to $20 a month, or $180-$200 a year, whereas a home insurance policy costs an average of $1,500 per year. Homeowners need to carry a sufficient amount of dwelling coverage to cover the cost of rebuilding their homes in the event it’s destroyed. Dwelling coverage does not include other structural damage or personal property damage, which is another set of costs to consider when calculating a home insurance premium, making home insurance more expensive than renters.

It’s essential to keep in mind that several factors can influence how much you pay for renters or homeowners insurance coverage, including:

- Amount of coverage needed

- Claims history

- Credit or insurance score

- Crime rate

- Deductible amount

- Location of home

Renters vs. Homeowners Insurance: Is It a Requirement?

Neither a home nor renters insurance policy is required by law but could be a stipulation in either a mortgage or lease agreement. Depending on your situation, you may be required to carry a specific amount of coverage.

Renters vs. Homeowners Insurance Discounts

Just about every carrier offers discounts for their policyholders. The most common discounts are:

- Bundling discount for multiple policies, including auto or motorcycle.

- Loyalty discount for being insured with the carrier for a specific time.

- Paid-in-full discounts for paying your premium in its entirety than in monthly installments.

- Safety discount for installing things such as burglar alarms or deadbolts.

Discounts are the obvious easiest way to save on renters or home insurance. Still, re-shopping your policy every year will yield the best results over time. The market is constantly evolving, and carriers must change their rates to compensate for inflation or increased natural disaster activity. Some carriers will raise their premiums by 30-40%, whereas some may see less than a 10% increase or even a decrease! Shopping your policy yearly at renewal will ensure you’re not overpaying for insurance and find you better coverage or a cheaper premium.

The easiest way to re-shop on home or renters insurance is to talk to one of our TGS Insurance agents. Our licensed team of experts will shop our book of over 40+ carriers to find you a policy perfectly balanced in coverage and price. The best part? We’ll re-shop your policy at every renewal, so you’ve always got the best the market offers.

Frequently Asked Questions

Can you have homeowners insurance and renters insurance?

Yes, you can have a homeowners and renters insurance policy simultaneously. Still, it’s unnecessary unless you rent an apartment AND own a home.

Does homeowners insurance cover rental property?

If you’re renting a home, you will need to purchase a renters insurance policy if stipulated in your lease agreement. However, suppose you rent out a home. In that case, you’d need to buy a landlord’s policy because a standard home insurance policy doesn’t cover rental situations due to the increased risk and liability.

Do I need home insurance for an apartment?

No, you do not need home insurance if you live in an apartment. The building is covered under the property owner’s landlord policy, and you would only need to purchase a renters insurance policy. If you own an apartment in a building, you may be required to have a condo policy.

Homeowners insurance for rental property cost?

Homeowners insurance typically does not offer coverage for rental property due to the increased risk of having tenants. Therefore a landlord’s policy could be needed. Depending on the location, type, and risk, a landlord policy is typically 20-25% more than a home insurance policy.

Instant Home Insurance Quote

Recent Home Insurance Articles:

- Thanksgiving Fire Safety: Protect Your Home, Your Family, and Your Peace of Mind

- Fall Home Maintenance Checklist: Prevent Costly Insurance Claims Before Winter

- Who Needs to be Listed on Homeowners Insurance

- Does Homeowners Insurance Cover Mold?

- Actual Cash Value vs. Replacement Value: What’s the Difference, and Where Does Market Value Fit In?