What is an Auto Insurance Deductible?

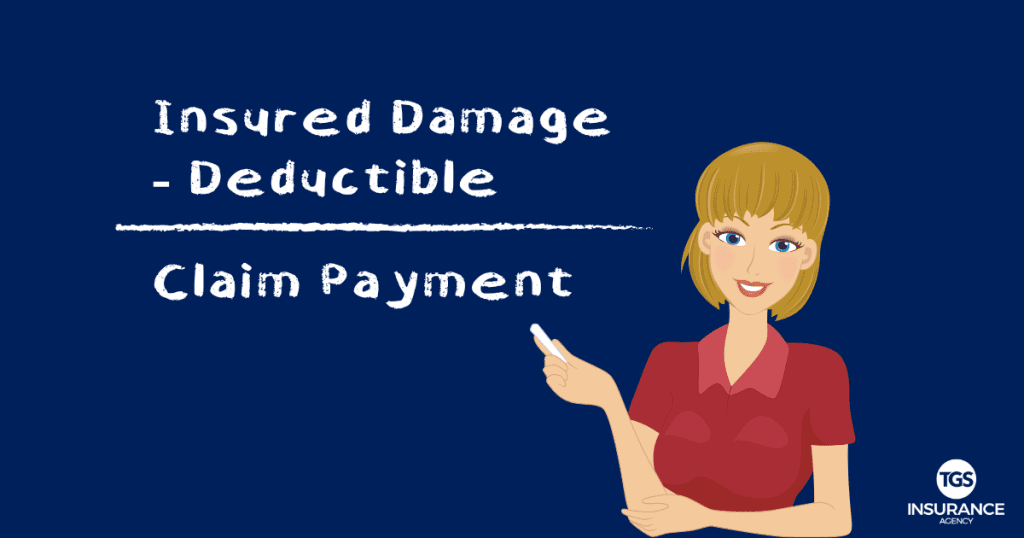

A car insurance deductible is the amount you’ll be held responsible for paying out of pocket for an accident before your insurance company will pay anything. Your deductible is subtracted from the estimated insured damage amount that you file a claim for; what you are left with is the claim payment you will receive from your carrier.

You choose your auto insurance deductible amount when you purchase your policy. The most popular car insurance deductible is $500, but it can vary based on your needs, your carrier, and where you live.

- If you choose a higher deductible, your premiums will be lower, but you have to keep in mind that you will be on the hook for a larger amount of money should you need to file a claim.

- If you choose a lower deductible, your monthly premiums will be higher, but you will not have to pay as much out of pocket if you file a claim.

Which Auto Insurance Coverage Types Have Deductibles?

Property Damage Liability Coverage: No, there is not a deductible.

Liability insurance never uses a deductible because it covers damage you cause to someone else’s property in an accident.

Bodily Injury Liability Coverage: No, there is not a deductible.

This also does not have a deductible because it covers injuries you caused to another person in a car accident.

Collision Coverage: Yes, there is a deductible.

There is almost always a deductible for collision coverage. This type of insurance covers you from accident, no matter who is at-fault.

Comprehensive Coverage: Yes, there is a deductible.

This type of insurance covers damage from situations that are out of your control like fires, floods, falling objects and vandalism.

Personal Injury Protection: Yes, there is a deductible.

This type of coverage helps to cover medical expenses for you and your passengers.

Uninsured Motorist Bodily Injury Coverage: No, there is not a deductible.

This coverage type does not usually require a deductible. This covers medical expenses that result in an accident if the at-fault driver does not have insurance or does not have enough insurance to cover the damages.

Uninsured Motorist Property Damage Coverage: Yes, there is a deductible.

This type of coverage provides compensation for damages to your property (your vehicle) after an accident with an uninsured driver or a driver without enough insurance to cover the damages.

Medical Payments Coverage: No, there is not a deductible.

MedPay coverage never has a deductible. It covers medical expenses after an accident.

| Coverage | Deductible |

| Property Damage Liability Coverage | No |

| Bodily Injury Liability Coverage | No |

| Collision Coverage | Yes |

| Comprehensive Coverage | Yes |

| Personal Injury Protection | Yes |

| Uninsured Motorist Bodily Injury Coverage | No |

| Uninsured Motorist Property Damage Coverage | Yes |

| Medical Payments Coverage | No |

When Do You Pay a Deductible for Car Insurance?

It is important to note that you will pay your deductible (for the appropriate coverage) every time you file a claim. Typically, you don’t have to write a check to your insurer, they simply subtract the deductible amount from your claim’s approved payout. For example, if you file a claim for $3,000 in damages and your deductible is $500, then your provider will give you $2,500 for the repairs.

What Is The Average Car Insurance Deductible in Texas?

Being in the Lone Star State makes us proud again! Texas’ car insurance premiums are well below the national average cost. This means that you are paying a lot less here than in other parts of the country. If you have all types of deductible-holding coverages on your auto insurance policy, then you should expect to add- on average- $578.

| Type of Coverage | Most Common Deductible Amount | Average Premium |

| Collision | $500 | $344 |

| Comprehensive | $500 | $186 |

| Uninsured/Underinsured Motorist Property Damage | $250 | $48 |

The higher your deductible, the lower your monthly premium.

Choosing your deductible can be tricky and a few things need to be taken into consideration. You will need to determine how much you are willing to pay out-of-pocket and, if you are in an accident, how likely are you to actually make a claim.

If you are at-fault for an accident, there isn’t much you can do to get out of paying your deductible for collision coverage.

In most cases, your car insurance provider will work directly with the repair shop. Once the repairs are complete, you will pay your deductible to the repair shop. Occasionally, the repair shop will offer payment plans if you can’t pay your deductible all at once.